Tiny Titans: Micro-Caps Gaining Momentum

This week, we cover James O’Shaughnessy’s Tiny Titans stock-picking strategy and give you a list of stocks currently passing the AAII O’Shaughnessy Tiny Titans screen based on the approach. The O’Shaughnessy Tiny Titans strategy focuses on micro-cap stocks that meet specific criteria for value, size and momentum.

For investors with patience and the ability to withstand the higher short-term volatility and risk of micro-cap stocks, there is potential for strong long-term returns. As of April 30, 2026, AAII’s O’Shaughnessy Tiny Titans screening model has an annual average gain since inception in 1998 of 26.0%, versus 7.4% for the S&P 500 index over the same period.

Investing in Micro-Cap Companies Using the O’Shaughnessy Tiny Titans Screen

AAII tracks several screens from O’Shaughnessy, the founder and chair of O’Shaughnessy Asset Management LLC, an asset management firm headquartered in Stamford, Connecticut. The O’Shaughnessy screens that AAII has developed are based on the strategies outlined in his books “What Works on Wall Street” (Fourth Edition, McGraw-Hill, 2011) and “Predicting the Markets of Tomorrow” (Penguin Group, 2006). It is from the latter book that the concept of the Tiny Titans approach was derived.

The Tiny Titans approach focuses on micro-cap stocks. Much research has been done regarding the success of investing in this market-capitalization category. AAII’s Model Shadow Stock Portfolio is based on a study showing that small- and micro-cap stocks tend to outperform the overall market over long periods.

O’Shaughnessy believes the reason for this outperformance is that few analysts follow these small stocks. Also, many institutional investors and mutual funds cannot trade these stocks without moving the price due to the relatively small number of outstanding shares. This leaves room for surprises, which can lead to a performance “pop.” O’Shaughnessy also says that micro-cap stocks have a low correlation with the overall stock market, making them a potential hedge in a portfolio of larger-cap stocks.

Low Price-to-Sales Ratio and Strong Price Strength Relative to the Market

AAII’s version of O’Shaughnessy’s Tiny Titans stock screen consists of very few criteria. First, all foreign and over-the-counter (OTC) stocks are eliminated. Next, a stock’s market cap must be between $25 million and $250 million.

After filtering out the larger-cap stocks, the Tiny Titans screen looks for stocks with price-to-sales (P/S) ratios of less than 1.00. The price-to-sales ratio compares the current stock price to the company’s sales per share. O’Shaughnessy uses this as a proxy for “cheapness,” as opposed to a price-earnings (P/E) ratio. He reasons that all viable companies have sales, and sales are harder to manipulate than earnings. In the third edition of “What Works on Wall Street,” O’Shaughnessy found that stocks with low price-to-sales ratios produced higher returns.

Finally, O’Shaughnessy thinks that investors should hold 25 stocks in this micro-cap portfolio to diversify the risk that goes along with investing in such volatile stocks. He narrowed his list to the 25 stocks with the highest 52-week relative strength compared to the S&P 500 index. Therefore, AAII tracks only those 25 companies with the highest 52-week relative strength each mont

For a stock investing strategy to be useful, it must be investable. That means that a quantitative approach needs to generate a large enough universe of passing companies on which to perform additional due diligence to identify investment candidates. Since the O’Shaughnessy Tiny Titans screen looks for the 25 companies with the highest price strength over the last year after applying the market-cap and value filters, there are always companies passing. Keep in mind, however, that there may be periods when the companies with the “best” price strength may still be down over the last 52 weeks. The Tiny Titans methodology looks for those companies with the strongest price performance, but not necessarily a positive price change.

Members are looking for your input. Can you help with this question from the Stock Screening & Analysis Community?

“How might you apply O’Shaughnessy’s multifactor approach to managing volatility and timing allocations during shifting long-term market cycles and mean-reversion phases?”

Click here and then choose the Join Community button on the right to answer this question or read their responses.

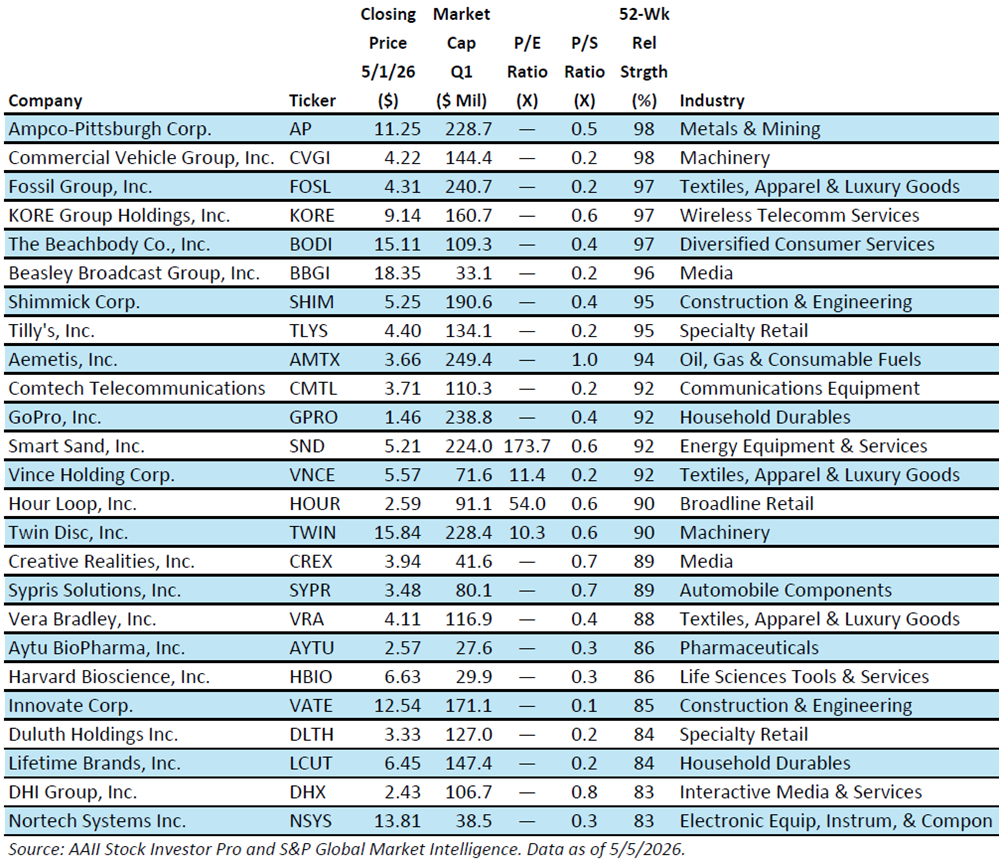

Tiny Titans Screen Criteria

Here is the full list of criteria used in conjunction with AAII’s Stock Investor Pro software to screen for stocks passing the O’Shaughnessy Tiny Titans screen:

Companies not based in the U.S. are excluded

Companies that trade on the OTC market are excluded

Market cap for the latest fiscal quarter (Q1) is greater than or equal to $25 million and is less than or equal to $250 million

The price-to-sales ratio is less than 1.00

The final results are the 25 companies with the highest relative price strength over the last 52 weeks

Stocks Passing the O’Shaughnessy Tiny Titans Screen (Ranked by 52-Week Relative Strength)

Keep in mind that no matter how well a stock screening methodology has performed (or how badly it has underperformed) over the long term, stock screening is only the first step in the stock selection process. You will want to do your homework to see why these companies are at their current levels. Only then will you gain insight into those that will continue to languish and those that may eventually flourish.

The stocks meeting the criteria of the approach do not represent a “recommended” or “buy” list. It is important to perform due diligence to verify the financial strength of the passing companies and to identify those stocks that match your investing tolerances and constraints before committing your investment dollars. Keep in mind that the quantitative screens AAII has developed are based upon our interpretations of published works tied to the market gurus.