The Stock Market at Midyear: Big Gains Fueled by Earnings Growth

As we gear up to celebrate the U.S.’ 250th Fourth of July (aka the semiquincentennial), the S&P 500 index is coming off its best quarterly gain in six years. The large-cap index surged 15.2% in the second quarter of 2026. The S&P SmallCap 600 index performed even better, soaring 19.7%.

Year to date, the S&P 500 has set 24 new all-time highs. This puts 2026 among the top 20 years since World War II for record highs set during the first half of the year, according to CFRA Research chief investment strategist Sam Stovall.

What is notable about the market’s run is that there is earnings growth behind it. Only three of the 11 S&P 500 sectors failed to report double-digit growth in first-quarter 2026, according to LSEG I/B/E/S. Large-cap consumer staples companies gained 8.1%. The energy and healthcare sectors reported declines of 0.8% and 3.4%, respectively.

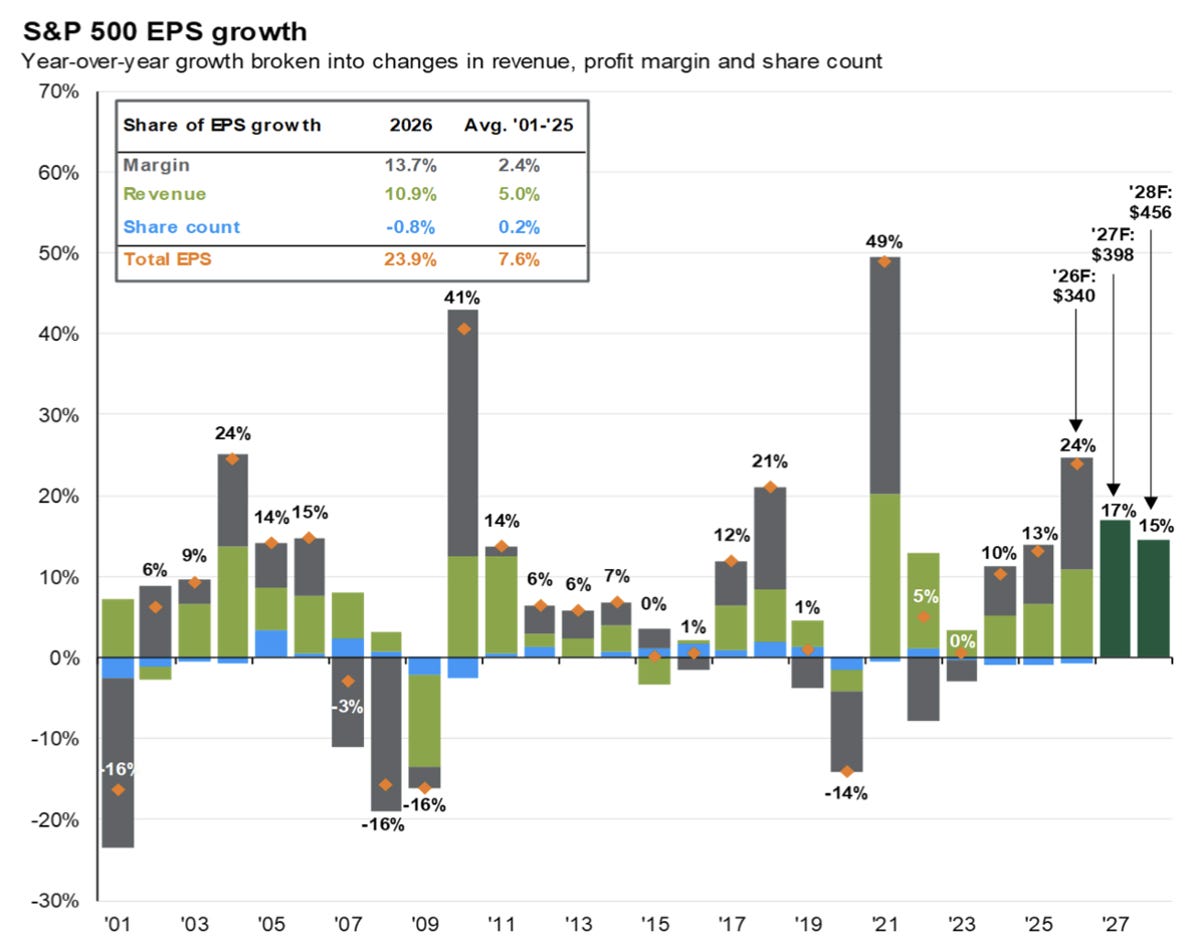

The earnings growth is being fueled by widening profit margins, as illustrated by the chart below from J.P. Morgan Asset Management’s Guide to the Markets. The gray shading in each column is the contribution of profit margins to growth.

Source: J.P. Morgan Asset Management.

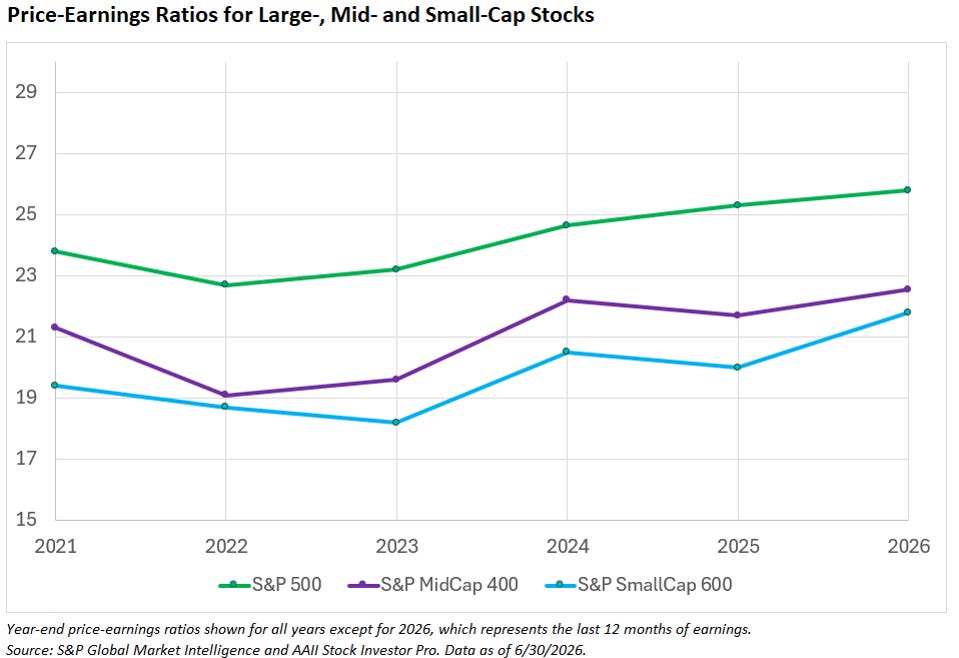

Valuations for the median stock have been rising, though at a slower pace than the price gains. The trailing 12-month price-earnings (P/E) ratio for the median S&P 500 stock is 25.8. The index’s five-year average price-earnings ratio is 23.9.

This isn’t to say that S&P 500 valuations are cheap, but it does show that we are not seeing a big multiple expansion. (Multiple expansion occurs when valuation ratios rise faster than the fundamental metric on which they are based.) This is a positive for the stock market. More attractive valuations continue to be found among mid-cap (median price-earnings ratio of 22.6) and small-cap (21.8) stocks.

Among the AAII Stock Screens, those incorporating growth or momentum measures fared best during the first half of the year. The Driehaus Revised screen soared 60.1% year to date. The original Driehaus screen ranks in second place with a 46.3% year-to-date return. Though both require recent accelerations in earnings growth, the revised screen also has relative strength criteria.

The outperformance of growth- and momentum-related screens is not surprising. The S&P 500 Momentum index and the S&P 500 Growth index were two of the best S&P 500 subindexes during the first half of 2026. They rose 44.1% and 21.9%, respectively.

Looking to the Second Half of 2026

Based on historical data, the 24 all-time highs set during the first half of the year are a lucky sign. In the other years ranking in the top 20 years for first-half record highs, the S&P 500 gained an additional 6% on average and rose in price 80% of the time in the second half of the year, according to Stovall.

Earnings growth lends support to these odds. Analyst forecasts compiled by LSEG I/B/E/S call for earnings to rise in the third and fourth quarters of 2026 for both S&P 500 and Russell 2000 index companies.

Valuations are not cheap, but they’re not excessive either. The median forward price-earnings ratio for S&P 500 companies is 19.0. Small-cap stocks are cheaper with a median forward price-earnings ratio of 16.0.

The geopolitical and macroeconomic pictures are wild cards. Though oil prices have come down, traffic in the Strait of Hormuz remains well below pre-war levels. Traders continue to price in the possibility of the Federal Reserve raising interest rates twice before the end of the year.

Downside volatility during the third quarter of a calendar year is not unusual. Pullbacks (declines of 5% to 10%) are a normal part of stock market behavior. Predicting their timing requires a working crystal ball.

Long-term, disciplined investors learn not to get giddy about bull market runs or anxious about market drops. Still, it is always more enjoyable when Mr. Market is in a good mood

Holiday Schedule

The U.S. financial markets and the AAII office will be closed on Friday, July 3, in observance of Independence Day. We at AAII wish you and your family a safe and enjoyable Fourth of July weekend.

More on AAII.com

Navigating Market Cycles With Shiller’s CAPE Ratio

The CAPE ratio empowers long-term investors to navigate volatile markets, forecast returns and make smarter decisions grounded in historical valuation trends.Driehaus Revised Screen

The “father of momentum investing,” Richard Driehaus, devised an approach that seeks out companies with accelerating earnings growth, rising earnings estimates and meaningful positive earnings surprises.Outperformance and 10 Changes for the Model Shadow Stock Portfolio

The newly released July 2026 AAII Journal includes a quarterly review of the model portfolio, which resulted in five deletions and five additions.

AAII Sentiment Survey

Optimism among individual investors about the short-term outlook for stocks decreased in the latest AAII Sentiment Survey. Meanwhile, neutral sentiment and pessimism increased.

Bullish sentiment, expectations that stock prices will rise over the next six months, decreased 13.6 percentage points to 31.4%. Bullish sentiment is below its historical average of 37.5% for the sixth time in seven weeks.

Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, increased 7.4 percentage points to 26.4%. Neutral sentiment is below its historical average of 31.5% for the 102nd time in 104 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, increased 6.1 percentage points to 42.3%. Pessimism is unusually high and is above its historical average of 31.0% for the 21st consecutive week.

The bull-bear spread (bullish minus bearish sentiment) decreased 19.7 percentage points to 10.9%. The bull-bear spread is below its historical average of 6.5% for the 19th time in 21 weeks.

This week’s special question asked AAII members if their portfolios are “all American,” or if they also diversify internationally [via stocks, exchange-traded funds (ETFs) and/or mutual funds]?

Here is how they responded:

Most of my portfolio is domestic, with just a small allocation to foreign companies: 54.5%

I hold a mix of domestic and foreign investments: 29.8%

I solely invest in domestic companies: 12.4%

Prefer not to answer: 1.7%

This week’s Sentiment Survey results:

Bullish: 31.4%, down 13.6 points

Neutral: 26.4%, up 7.4 points

Bearish: 42.3%, up 6.1 points

Historical averages:

Bullish: 37.5%

Neutral: 31.5%

Bearish: 31.0%