Opportunities for Donor-Advised Funds Opened by the OBBBA

How donor-advised funds work and key considerations before contributing assets

Changes under the OBBBA affecting deductions and giving strategies

How strategies like bunching can maximize charitable impact and tax efficiency

The One Big Beautiful Bill Act (OBBBA) of 2025 enacted important changes for charitably minded and tax-averse households. Donor-advised funds (DAFs) continue to be a compelling philanthropic tool for high-net-worth households. Here we examine how donor-advised funds are structured, who might find them attractive and why, and what changes were introduced by the OBBBA.

Donor-advised funds allow households to generate immediate tax deductions by donating money or assets to the fund. The charitable organizations that sponsor donor-advised funds administer funds that are divided into individual subaccounts. Those accounts accept donations and disburse gifts on a donor’s behalf. Unlike many other giving options, donor-advised funds allow donors to make anonymous grants to avoid being put on solicitation lists.

Funds frequently offer donor-directed investment options that can help your gift grow or earn tax-free income. Advances in financial technology over the years have made donor-advised funds even more convenient and flexible.

The three largest sponsors of donor-advised funds are Fidelity Charitable, National Philanthropic Trust and DAFgiving360 (which was spun off from Charles Schwab in 2024). Vanguard Charitable is also included in our discussion here, given Vanguard’s popularity as an investment manager. Although the sponsors may be charitable entities, donor-advised funds are often related to large financial services firms because they can invest assets in funds that generate management fees for the investment adviser.

Donations to donor-advised funds now outpace donations to individual charities. For example, according to 2023 data from the Institute for Policy Studies, Fidelity Charitable received approximately two-and-one-half times the donations reported by the largest individual charity, Feeding America.

What You Need to Know Before Funding

Donations to a donor-advised fund are irrevocable. Once you deposit money, it becomes an asset owned by the fund until it is granted to your approved charities. Depending on the fund sponsor’s requirements, donations may be in the form of stock, cash, cryptocurrency and/or illiquid assets such as appreciated real estate and private business interests.

Such donations are beneficial from a tax standpoint. Capital gains taxes on an appreciated asset are avoided when that asset is contributed to a donor-advised fund. Additionally, the taxable deduction is generally based on the donated asset’s market value at the time of the donation. This amount can be significantly higher than the price originally paid for the asset.

The type of asset and your adjusted gross income (AGI) dictate how much of a tax deduction is available. For example, deductions for appreciated property such as collectibles are capped at 30% of your contribution base. Any excess can be carried forward for five years.

A donor-advised fund must ensure that its grants go to qualifying purposes to keep its nonprofit 501(c)(3) exemption. Because of that, donors may only advise where the sponsor directs funds. The expectation is that the donor-advised fund will honor any donor recommendation that follows the fund’s guidelines.

The Internal Revenue Service (IRS) has specific rules on what qualifies as a charity. Political candidates, organizations and individuals are not considered charities. Qualifying purposes are:

“… charitable, religious, educational, scientific, literary, testing for public safety, fostering national or international amateur sports competition, and preventing cruelty to children or animals. The term charitable is used in its generally accepted legal sense and includes relief of the poor, the distressed, or the underprivileged; advancement of religion; advancement of education or science; erecting or maintaining public buildings, monuments, or works; lessening the burdens of government; lessening neighborhood tensions; eliminating prejudice and discrimination; defending human and civil rights secured by law; and combating community deterioration and juvenile delinquency.”

Donors, advisers to donors and related persons cannot receive anything other than an incidental benefit from a donor-advised fund, otherwise costly excise taxes apply. Tickets to events, memberships and dinners are some examples of prohibited benefits.

Contribution and Distribution Minimums

Each donor-advised fund sponsor has its own rules regarding contributions and distributions. As shown in Table 1, both Fidelity Charitable and DAFgiving360 allow a donor-advised fund to be set up for any dollar amount. National Philanthropic Trust requires a minimum $10,000 contribution, while Vanguard Charitable sets its minimum at $25,000.

Distribution rules also vary. Fidelity Charitable and DAFgiving360 allow for grants as little as $50 to be made. National Philanthropic Trust has a $250 per grant minimum, while Vanguard Charitable requires grants to be at least $500.

Beyond the grant size, pay attention to the rules about how often grants must be made. Fidelity Charitable, for instance, requires that at least one grant be made every two years. If this requirement is not met, Fidelity Charitable uses the donor’s fund to make a grant to a charitable organization of its choice.

Read the sponsor’s rules regarding grants before opening a donor-advised fund.

Investment Options for Tax-Exempt Growth and Income

Account holders may invest for tax-exempt growth and/or income, which can leverage the impact on their charities. Each sponsor has its own menu of investment options, like company 401(k) plans. Larger accounts might be able to add hedge funds, private equity and other alternatives with the sponsor’s approval.

DAFgiving360 has pools for index and actively managed growth; balanced, conservative and socially responsible investing pools; international pools; fixed-income options; and money market pools. Fidelity Charitable and Vanguard Charitable have similar offerings. Along with traditional options, National Philanthropic Trust has a wide array of impact investing funds, which screen investments according to additional criteria, such as investing in accessible housing, disaster relief and economic opportunity.

Some sponsors permit delegating investment responsibilities to an outside adviser and hold the assets in a segregated account. Investors may want this option to maintain a relationship with someone they trust or to continue a preferred investing strategy.

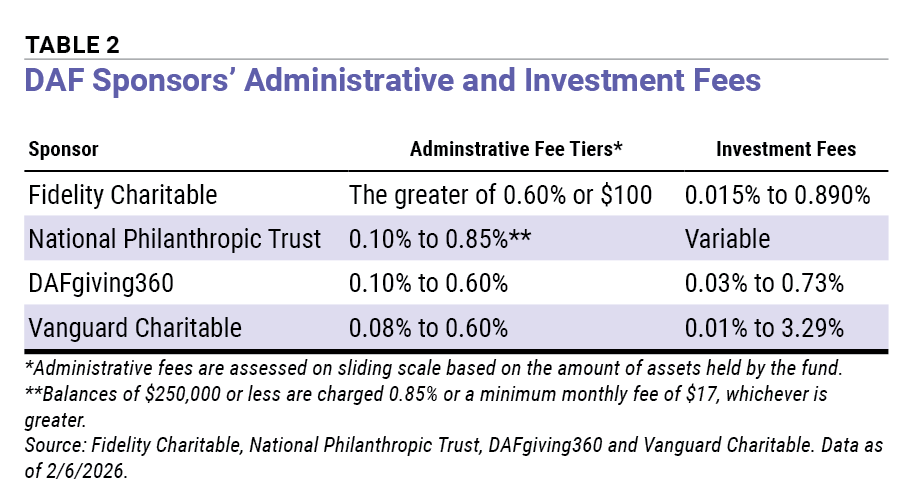

How Much Does a Donor-Advised Fund Cost?

There are two primary types of fees charged by donor-advised funds.

The first is an administrative fee. This fee covers the cost of servicing the donor-advised fund. Administrative fees are charged on a sliding scale based on the size of the donor-advised fund. The larger your fund is, the lower your fee will be on a percentage basis.

Again, read the fine print before picking a sponsor. National Philanthropic Trust charges a flat monthly fee of $17 for donor-advised funds that hold less than $250,000 in assets.

The second type of fee is investment fees. These are the expense ratios for each investment you choose. They vary by both sponsor and type of investment.

Vanguard Charitable describes its available investment options as having an average expense ratio of 0.04%. While most of the options do have very low expense ratios, its Private Assets Fund charges a hefty 3.29%.

Table 2 compares both the administrative and investment fees across the primary donor-advised fund sponsors.

Changes to Giving Under the New Tax Law

The OBBBA put a few twists into the giving game. There’s good news for taxpayers who take the standard deduction. Beginning with the 2026 tax year, you can get up to $1,000 of additional deductions ($2,000 if married filing jointly) for donating cash directly to a charity. If you plan to donate that amount or less, this is likely the best option. Don’t forget to get a receipt.

If you itemize your taxes, the math is a bit more complicated. Charitable gifts must now exceed a floor of 0.5% of your contribution base (typically AGI) before they may be deducted. For example, a couple with adjusted gross income of $100,000 who deposit $10,000 into their donor-advised fund this year would only be able to deduct $9,500 on their 2026 tax return. The remaining $500 deduction can be carried forward for up to five years, subject to meeting the floor test in future years.

Taxpayers in the highest 37% tax bracket (taxable income of at least $768,700 married joint/$640,600 single in 2026) will also see their total itemized deductions lowered by 2/37ths (5.4%). This effectively caps the benefit of all itemized deductions, including charitable donations, at 35% instead of 37%.

Bunching Can Help Navigate the New Floor on Deductions

Susie is a generous supporter of her local library foundation and likes to donate $3,000 each year. She has an AGI of $100,000, which establishes a $500 floor ($100,000 × 0.5%) before she may claim a deduction. If she donates $3,000 each year to a donor-advised fund, she would only be able to deduct $2,500, which is about 80% of her donation.

Rather than giving annually, she can “bunch” her gifts in advance and make annual grants from the donor-advised fund account. If she donates $15,000 in one year, she could deduct $14,500 that year. Then she can recommend that the donor-advised fund send recurring $3,000 grants for the next five years.

Combining Bunching With Regular Charitable Giving

Heather wants to support the University of Michigan’s Wolverines, her favorite football team, by donating $5,000 to their football program every year that they have a winning season. The University of Michigan has a 501(c)(3) charity to receive donations. There are a few local 501(c)(3) charities she’s also open to donating to, but she’s mainly passionate about the Wolverines.

Heather’s wealth comes from an actively managed stock portfolio with some substantial gains and losses, leading to wide swings in capital gains tax liability from year to year. Her children graduated from Michigan State University and don’t feel the same allegiance to the Wolverines as she does. Heather wants to donate enough each year to minimize her taxes.

If she donated $5,000 to her donor-advised fund account every year that the University of Michigan crushed it, she might be donating in years when she has a lower tax liability. She also might have years when she could use a much larger tax deduction. If she sold stocks with capital gains to fund her cash gifts, she would increase her taxes.

Both a private foundation and a donor-advised fund would allow Heather to address both her philanthropy and her desire to minimize her taxes, but a donor-advised fund is the better option. First, setting up a private foundation to accomplish a very specific goal seems needlessly expensive. Second, a private foundation is required to distribute 5% of its assets every year, which might become an issue when the Wolverines fail to notch enough wins in a season.

Heather should consider establishing an account with a donor-advised fund and funding it with highly appreciated stock in the years she has a high tax liability. This would allow her to avoid paying any capital gains on those stocks. In addition, if she has held the stocks for more than 12 months, she can deduct their full fair market value rather than just her cost basis.

She will have to pay attention to the 30% ceiling on deducting charitable donations of appreciated stocks—contributions cannot exceed 30% of her adjusted gross income in any single year. However, any excess amounts can be carried forward for up to five years.

Even with these restrictions and ceilings, combining bunching with a donor-advised fund is powerful. Heather is able to claim tax deductions on her charitable giving during the years they would benefit her most, sidestep capital gains taxes, and still limit her donations to the Wolverines to only the years when they have a winning season.

Because sponsors often have minimum disbursement requirements and the Wolverines could have a multiyear slump, Heather might want to designate one or more of her other favored charities to receive a contribution every year.

Legacy Planning for Donor-Advised Funds

Donor-advised funds also provide the option of giving after death.

Heather, for instance, should consider how she wants the account to be handled upon her death. If she does not leave instructions, the account’s assets will be disbursed or held according to the sponsor’s policies.

Donor-advised funds allow accountholders to appoint successors who assume responsibility for making grants. Note that the successor is not bound by the deceased account holder’s preferences. Depending on the sponsor, account holders can also list beneficiary charities (not individuals) who will receive lump sums or periodic payments.

“As I Give, I Get”

Perhaps no better quote (commonly attributed to Mary McLeod Bethune) describes the benefits of philanthropy. Giving not only helps others—it nourishes donors’ hearts. Along with enriching your spirit, selecting the right vehicle for your charitable efforts can boost your legacy.

When used properly, donor-advised funds allow donors to align their gifts with their tax situation. Then they can position those assets for tax-exempt growth or income and make grants according to the charities’ needs or the donor’s preference, all in a convenient account.