Mutual Funds to Gain ETF Tax Advantages and Intraday Trading

DFA’s DFSV and DFSVX may soon share ETF tax benefits as the SEC considers dual share classes. Discover what this change means for investors in mutual funds and ETFs.

The line separating exchange-traded funds (ETFs) and mutual funds could become much more blurred in the coming months. The U.S. Securities and Exchange Commission (SEC) issued a notice on Tuesday stating its intent to grant Dimensional Fund Advisors (DFA) the ability to offer ETF share classes for its existing mutual funds. This could create advantages for individual investors.

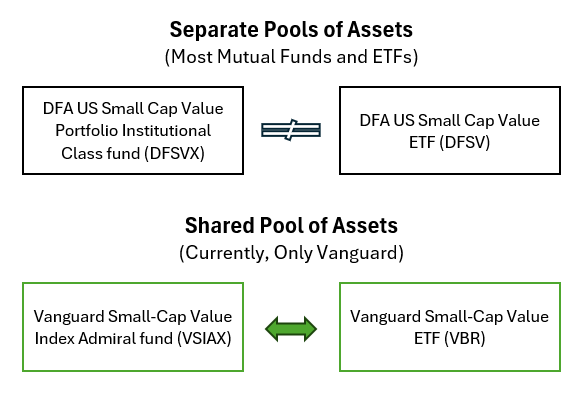

Currently, the ETFs and mutual funds offered by nearly all firms are separate entities. For instance, there is no intermingling of DFA US Small Cap Value Portfolio Institutional Class fund (DFSVX) assets and DFA US Small Cap Value ETF (DFSV) assets. They are two completely different investment vehicles. Purchases and redemptions made in the small-cap value mutual fund have no impact on the ETF with the same name.

Vanguard is the exception. Vanguard Small-Cap Value Index Admiral fund (VSIAX) and Vanguard Small-Cap Value ETF (VBR) are merely different share classes of the same fund. They share the same pool of assets. Inflows and outflows from the mutual fund share class affect the ETF share class, and vice versa.

A patent allowed Vanguard to be the sole fund family to do this for more than 20 years. This patent expired in 2023. Since then, applications from other investment firms to offer ETF classes for existing mutual funds have poured in. Morningstar says that over 75 firms have filed applications; Reuters puts the number at “about 80.”

DFA’s application says that shareholders will be able to exchange their mutual fund share classes for ETF share classes once the dual share classes are available. This will allow investors to get the tax benefits of ETFs without incurring capital gains taxes or any potential transaction fees.

Mutual fund share class holders should, in theory, gain some tax efficiency from the dual share class structure too. It would allow some portfolio changes to be conducted through the ETF share classes.

ETFs do in-kind transactions. An in-kind transaction frequently avoids being a taxable event because securities are swapped for other assets of equal value. Mutual funds, conversely, sell the assets that the managers want to remove from the portfolio. This can lead to capital gains, which are taxable.

Individual investors could also realize some cost savings when buying or selling fund shares. Currently, brokers limit the number of mutual funds that can be bought or sold on a transaction-free basis. All ETFs are bought and sold on a commission-free basis at most brokers.

However, there are potential downsides. The extent to which the dollar value of the assets associated with the mutual fund share is larger than that associated with the ETF class, the tax efficiency of the ETF could be adversely affected. For example, if many mutual fund shareholders redeem at once, the fund might need to sell securities for cash rather than execute tax-efficient in-kind transfers, potentially triggering capital gains for all shareholders, including ETF holders.

ETF shares could also trade at prices separate from their underlying net asset value (NAV). The ETF’s share price may be higher or lower than the underlying value of the assets attributed to each share. We already see this occurring with lesser-traded ETFs.

Capacity is another issue. When a manager believes their fund has reached its dollar limit for what it can attractively invest, they can close the fund. Closing off a fund to new inflows prevents investors from buying new shares in the mutual fund. ETFs cannot do the same. A flood of assets into a top-performing ETF could lead to too much money chasing too few assets.

Despite these risks, I think allowing more investment firms to offer dual mutual fund and ETF share classes is a win for us individual investors. It will give us a more tax-friendly investment structure, the flexibility to make portfolio changes during market hours (via the ETF share class) and lower costs. The change should also put more pressure on mutual fund companies to stop charging front-end loads.

What it does not do is resolve the problem of underperforming active fund managers, the higher fees charged by many funds or the risks of individual investors buying and selling too frequently.

AAII Sentiment Survey: October 3, 2025

Optimism among individual investors about the short-term outlook for stocks increased in the latest AAII Sentiment Survey. Meanwhile, neutral sentiment decreased and pessimism was unchanged.

Bullish sentiment, expectations that stock prices will rise over the next six months, increased 1.2 percentage points to 42.9%. Bullish sentiment is above its historical average of 37.5% for the third time in nine weeks.

Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, decreased 1.1 percentage points to 17.9%. Neutral sentiment is unusually low and is below its historical average of 31.5% for the 63rd time in 65 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, was unchanged at 39.2%. Bearish sentiment is above its historical average of 31.0% for the 44th time in 46 weeks.

The bull-bear spread (bullish minus bearish sentiment) increased 1.2 percentage points to 3.8%. The bull-bear spread is below its historical average of 6.5% for the 33rd time in 35 weeks.

This week’s special question asked AAII members if they hold gold or other precious metals in their portfolio, either directly or through an exchange-traded fund (ETF).

Here is how they responded:

No, I do not: 55.6%

Yes, I own gold or other precious metals: 18.7%

Yes, I own both precious metals and mining companies: 15.9%

I just own mining companies that focus on precious metals: 7.9%

I am considering adding gold to my portfolio: 1.9%

This week’s Sentiment Survey results:

Bullish: 42.9%, up 1.2 points

Neutral: 17.9%, down 1.1 points

Bearish: 39.2%, down 0.0 points

Historical averages:

Bullish: 37.5%

Neutral: 31.5%

Bearish: 31.0%

See more Sentiment Survey results.

AAII Asset Allocation Survey

Individual investors’ allocations to stocks increased while bond allocations increased and cash allocations decreased in the September AAII Asset Allocation Survey.

Stock and stock fund allocations increased 1.0 percentage points to 68.3%. Stock and stock fund allocations are above their historical average of 61.5% for the 64th consecutive month.

Bond and bond fund allocations increased 0.1 percentage points to 16.3%. Bond and bond fund allocations are above their historical average of 16.0% for the fourth time in six months.

Cash allocations decreased 1.1 percentage points to 15.4%. Cash allocations are below their historical average of 22.5% for the 34th consecutive month.

September AAII Asset Allocation Survey results:

Stocks and Stock Funds: 68.3%, up 1.0 percentage points

Bonds and Bond Funds: 16.3%, up 0.0 percentage points

Cash: 15.4%, down 1.1 percentage points

September AAII Asset Allocation Details:

Stocks: 28.4%, down 0.6 percentage points

Stocks Funds: 39.9%, up 1.6 percentage points

Bonds: 5.0%, down 0.5 percentage points

Bond Funds: 11.2%, up 0.6 percentage points

Historical averages:

Stocks/Stock Funds: 61.5%

Bonds/Bond Funds: 16.0%

Cash: 22.5%

Take the Asset Allocation Survey.

Investor Update Archives

September 25, 2025 Options for Your Cash as More Fed Rate Cuts Are Likely

September 18, 2025 September Charts of Interest: Rate Cuts, Plus a 3,821% Investment Return

September 11, 2025 Muni Bond Funds’ Additional Advantage

September 4, 2025 Beware of the Popularity Trap for ETFs