May Charts of Interest: What's Driving This Spring's Rally

This spring’s jump in the stock market has been strong. In this month’s charts of interest, we look at the two drivers behind the strength: corporate earnings and semiconductor stocks. We then switch to inflation before ending with a look at the tightening competitive race in artificial intelligence (AI).

As a reminder, the monthly charts of interest highlight charts and tables I’ve come across that have not made their way into other AAII commentaries.

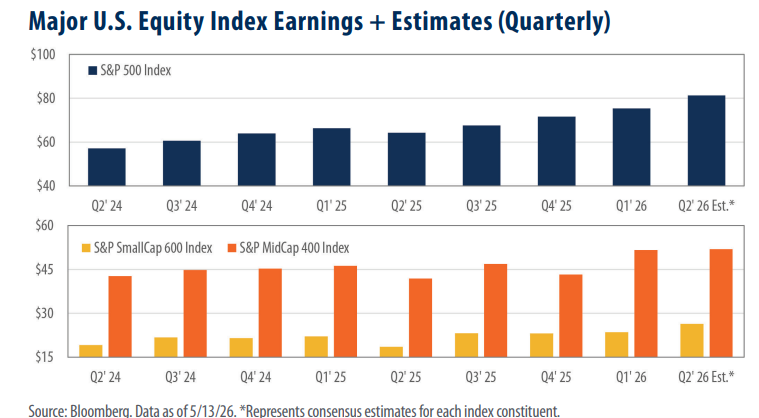

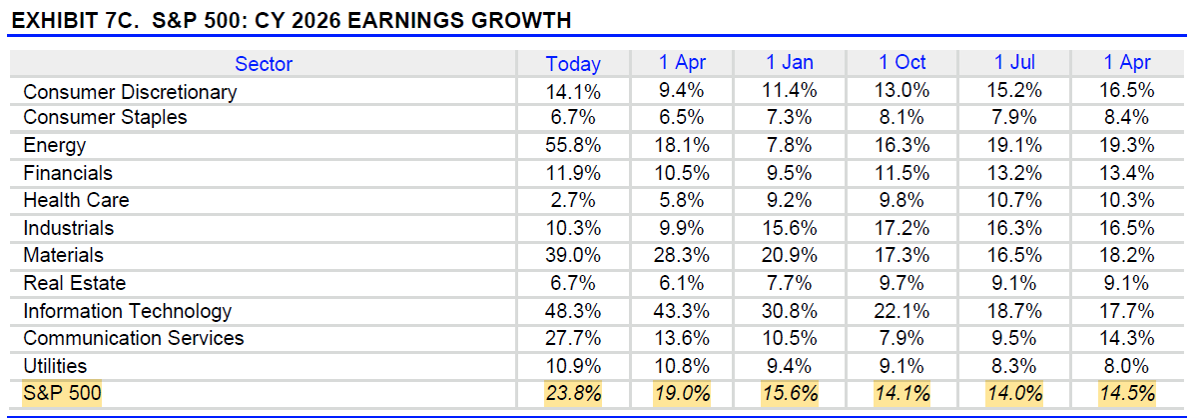

First-Quarter 2026 Earnings Have Been Good

Earnings have been a driver of this spring’s market rally. Corporations are reporting profit growth, and analysts have been upwardly revising their second-quarter and full-year 2026 earnings forecasts. First Trust Portfolios’ Robert Carey and Peter Leonteos shared this takeaway: “The S&P 500 index’s trailing 12-month price return of 30.6% [through May 8, 2026] nearly matches its [first-quarter 2026] year-over-year earnings growth rate of 27.7% as of the same date.”

The energy sector has influenced the upwardly revised full-year 2026 earnings estimates for the S&P 500, but it is not the only one. Analysts have also become more optimistic about the outlook for information technology and communication services companies. On the other hand, earnings growth expectations have fallen for the healthcare sector, per LSEG I/B/E/S.

Source: LSEG I/B/E/S. Data as of 5/15/2026.

Talk About Pushing Your Chips In

Nvidia Corp.’s (NVDA) run toward a $6 trillion market capitalization has played a role in helping the S&P 500 reach new highs, but it is not alone. Many other semiconductor stocks have also computed big gains lately. I plotted State Street SPDR S&P Semiconductor ETF (XSD) against iShares Core S&P 500 ETF (IVV). The semiconductor ETF tracks a modified equal-weighted index, which keeps Nvidia from having outsized influence on its performance. It is up significantly since the end of March.

Source: AAII.com. Data from QuoteMedia as of 5/20/2026.

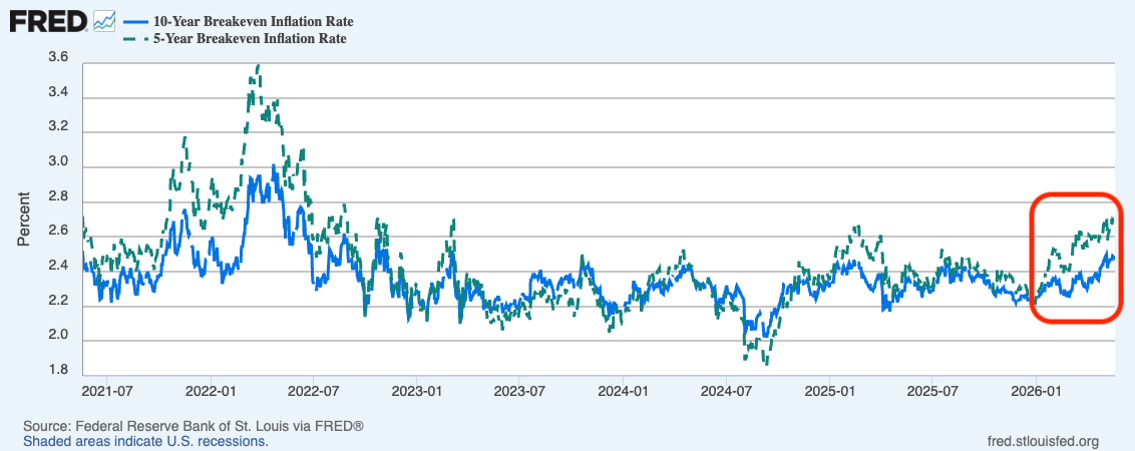

Inflation Expectations Are Rising

Incoming Federal Reserve chairman Kevin Warsh is not walking into an ideal inflation environment. On Tuesday, May 19, the five-year breakeven inflation rate was 2.66% —its highest level in three years. The 10-year breakeven rate is also rising. Both reflect the inflation expectations that traders are pricing into bonds. Blame the ongoing oil shock caused by the closing of the Strait of Hormuz.

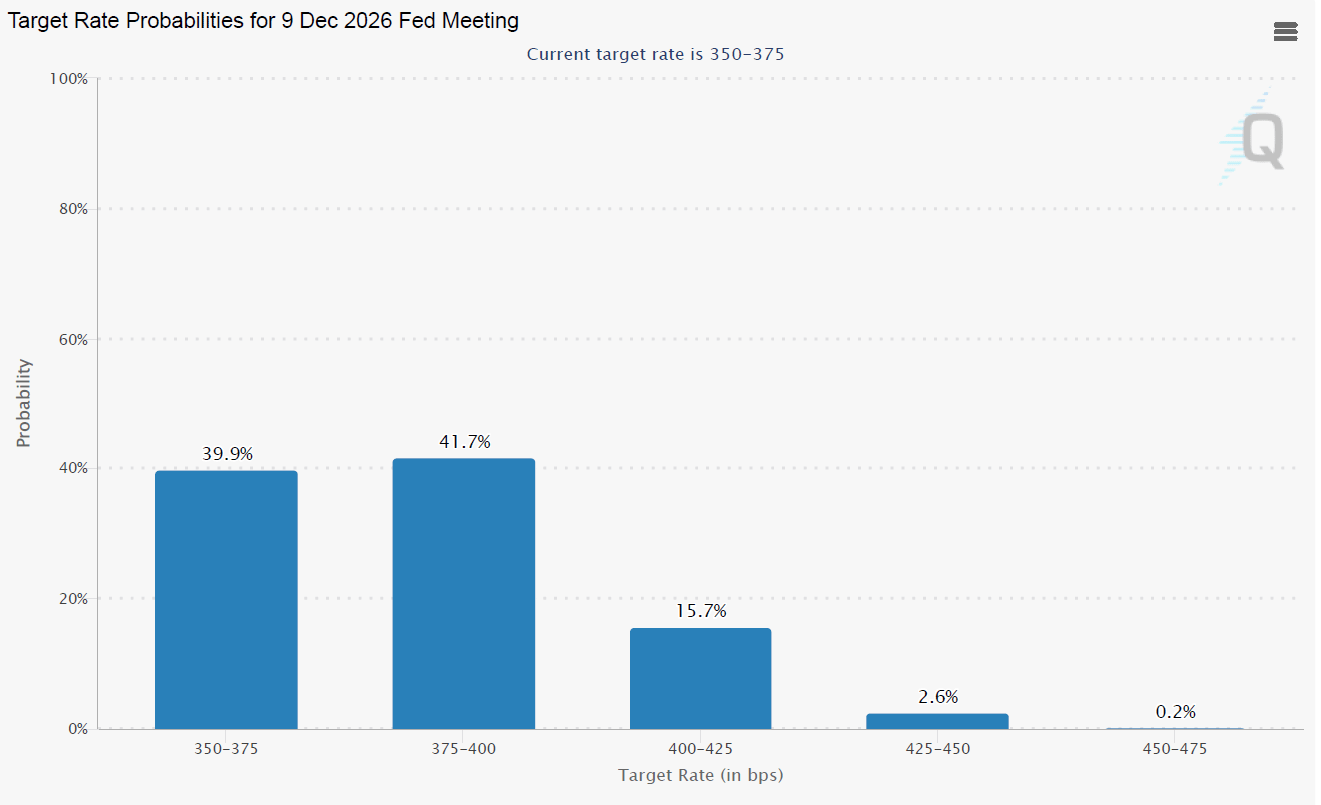

Will There Be an Interest Rate Hike Later This Year?

Given what’s happening in the bond market, at the gas pump and even with tomato prices (up 39% over the last year!), I revisited the CME FedWatch Tool. Traders are currently pricing in an approximately 60% chance of interest rates being raised by the end of this year. These odds could change significantly based on what does and does not happen with the Iran war.

Source: CME Group.

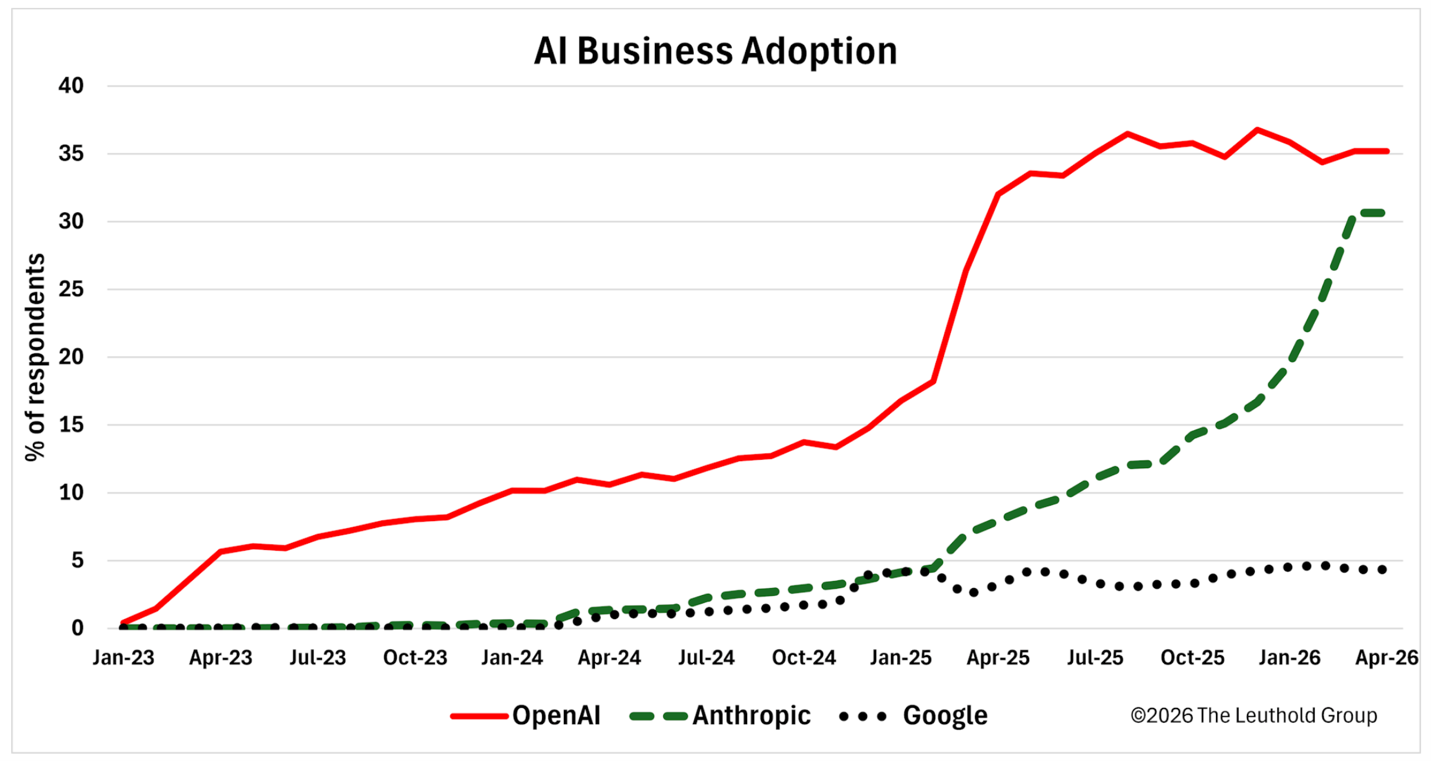

Traditional Business Forces Apply to AI Too

OpenAI, the company behind ChatGPT, is preparing to file for an initial public offering (IPO) “in the coming days or weeks,” according to The Wall Street Journal. The company will be questioned about whether it can maintain its current market share as it makes pitches to potential investors. Competitor Anthropic (the company behind Claude) has been gaining market share. Alphabet Inc.’s (GOOGL) Google Gemini has made inroads too.

The chart below from The Leuthold Group is a reminder that the still-young AI market is not immune from the traditional business forces of competition. The early entrants in technological innovation aren’t always the long-term winners.

More on AAII.com

How to Analyze Corporate Earnings in Five Steps

Earnings reports provide a snapshot of business performance, but they are most valuable when viewed as part of a longer-term trend.Incorporating Equal-Weighted Funds Into Your Allocation

Equal-weighted funds hold the same securities as similar market-cap-weighted funds but in different proportions, reducing stock-specific risk.Navigating the Rise of Prediction Markets

Participating in prediction markets should be regarded as speculative due to their binary outcomes, novel nature, evolving regulation, relatively high costs and low liquidity, as discussed in the May 2026 AAII Journal.

AAII Sentiment Survey

Optimism among individual investors about the short-term outlook for stocks decreased in the latest AAII Sentiment Survey. Meanwhile, neutral sentiment and pessimism increased.

Bullish sentiment, expectations that stock prices will rise over the next six months, decreased 7.6 percentage points to 31.7%. Bullish sentiment is below its historical average of 37.5% for the first time in five weeks.

Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, increased 0.6 percentage points to 24.7%. Neutral sentiment is below its historical average of 31.5% for the 96th time in 98 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, increased 7.0 percentage points to 43.6%. Bearish sentiment is unusually high and is above its historical average of 31.0% for the 15th consecutive week.

The bull-bear spread (bullish minus bearish sentiment) decreased 14.6 percentage points to –11.9%. The bull-bear spread is unusually low and is below its historical average of 6.5% for the 14th time in 15 weeks.

This week’s special question asked AAII members how they would describe the earnings guidance given by companies during first-quarter 2026 earnings season.

Here is how they responded:

Better than I expected: 51.9%

Approximately what I expected: 27.6%

Worse than I expected: 2.8%

Not sure/no opinion: 17.7%

This week’s Sentiment Survey results:

Bullish: 31.7%, down 7.6 points

Neutral: 24.7%, up 0.6 points

Bearish: 43.6%, up 7.0 points

Historical averages:

Bullish: 37.5%

Neutral: 31.5%

Bearish: 31.0%

See more Sentiment Survey results.

AAII Asset Allocation Survey

Individual investors’ allocations to cash increased while stock and bond allocations decreased in the April AAII Asset Allocation Survey.

Stock and stock fund allocations decreased 0.7 percentage points to 68.5%. Stock and stock fund allocations are above their historical average of 61.5% for the 71st consecutive month.

Bond and bond fund allocations decreased 0.2 percentage points to 15.6%. Bond and bond fund allocations are below their historical average of 16.0% for the sixth time in seven months.

Cash allocations increased by 0.9 percentage points to 15.9%. Cash allocations are below their historical average of 22.5% for the 41st consecutive month.

April AAII Asset Allocation Survey results:

Stocks and Stock Funds: 68.5%, down 0.7 percentage points

Bonds and Bond Funds: 15.6%, down 0.2 percentage points

Cash: 15.9%, up 0.9 percentage points

April AAII Asset Allocation Details:

Stocks: 29.5%, up 0.1 percentage points

Stocks Funds: 39.0%, down 0.7 percentage points

Bonds: 4.6%, down 0.5 percentage points

Bond Funds: 11.0%, up 0.3 percentage points

Historical averages:

Stocks/Stock Funds: 61.5%

Bonds/Bond Funds: 16.0%

Cash: 22.5%

Take the Asset Allocation Survey.