History Shows Investors Benefit From Staying Put During Crises

Special Note: My Portfolio will fully transition to the brand new AAII Investor Hub on March 15. The legacy My Portfolio interface will no longer be available at that point. This change is being made so we can add new features to the AAII Investor Hub, including broker integration with the fully rebuilt My Portfolio. All of your portfolios, your saved stock screens and your saved articles are currently on the Hub. We encourage you to start using the AAII Investor Hub today.

The strikes against Iran have led to a jump in oil prices and stock market volatility. There are big known unknowns that traders are attempting to price in. What we do know is that sticking with your portfolio allocation during periods of crisis has historically been the right move.

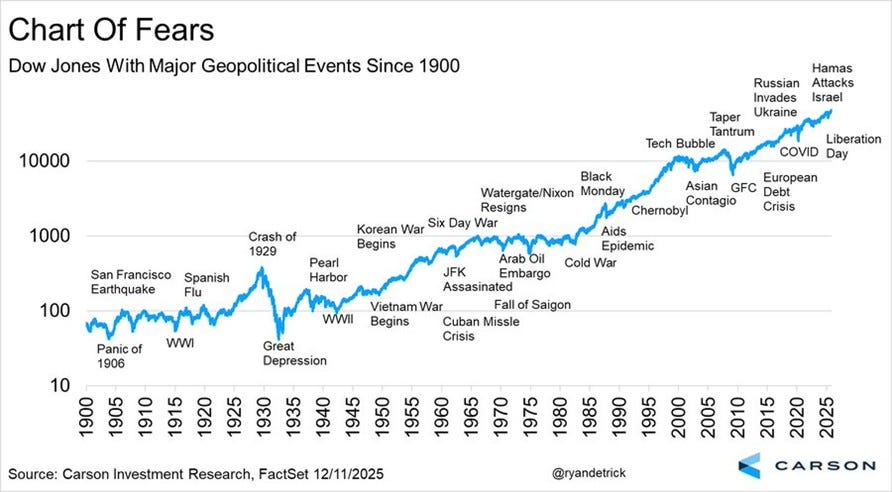

The stock market’s typical pattern following the start of a geopolitical event or other crisis has been to have an initial reaction and then move past it. The chart below from Ryan Detrick, CMT, at Carson Group shows how the Dow Jones industrial average has performed following major geopolitical events dating back to 1900. I chose this chart because it is updated through 2025.

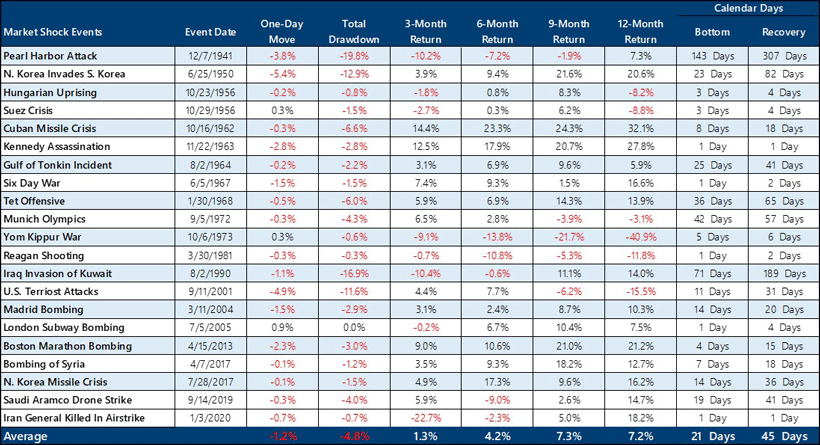

For those of you who prefer more detail, I include a table at the end of this article that I originally shared at the start of Russia’s invasion of Ukraine in 2022. It was put together by Calamos Wealth Management’s Investment Strategy Group and shows the stock market’s response to geopolitical conflicts dating back to World War II. The average total drop (aka drawdown) in the S&P 500 index from an event date to market bottom was 4.8%.

Averages are influenced by the upper and lower ends of the data. The S&P 500 plunged 19.8% following the 1941 attack on Pearl Harbor. It barely budged after Iranian general Qasem Soleimani was killed in 2020. The S&P 500’s 0.7% decline that day was within the realm of typical daily volatility.

While the day’s events always drive the headlines we see and the news we hear, patient investors know to think longer term. This behavior is to their benefit. After periods of six months or longer, factors beyond the immediate start or escalation of conflict have historically influenced the market’s direction.

Just as was the case when Russia invaded Ukraine, there are several known unknowns now. Iran has responded by attacking several countries. It is also in the process of naming a new leader. Shipments of oil through the Strait of Hormuz have dropped over 80%, according to The Wall Street Journal. How long the current military campaign will last and what comes after it are big question marks. Ideally, the Iranian government will be willing to compromise on its weapons, stop supporting terrorist groups and treat its own citizens better. (To paraphrase John Lennon, call me a dreamer, but I’m not the only one.)

Economically, the conflict’s impact goes beyond oil and natural gas. Cargo ships are reportedly rerouting to avoid Middle Eastern passageways like the Suez Canal. This extends transit times.

Many other factors could influence the direction of the global equity, fixed-income and commodity markets. The U.S. will soon be getting a new Federal Reserve chairman. We still lack certainty about tariffs. The European Union (EU) is both looking at new trade pacts and strengthening its military capabilities. Questions about artificial intelligence (AI) abound, both in terms of its broad impact and the level of investment in it. Other military conflicts could break out.

As investors, we don’t get to choose the financial market conditions we live through, much less the geopolitical conditions. Systematic risk—that is, the risk of doing anything with your money—never goes away. But the bigger risk to most investors’ portfolios is behavioral: making big portfolio decisions based on short-term events instead of staying focused on achieving longer-term financial goals.

Source: LPL Research, S&P Dow Jones Indices, CFRA, Bloomberg. Past performance doesn’t guarantee future results. The illustrated returns are reflective of the performance under the stated timeframe for the S&P 500 Index and beginning with the “event date”. The S&P 500 index is a stock market index that tracks performance of 500 U.S.-based large-cap companies from various sectors. It is widely considered a gauge of investor sentiment and its returns reflect the state of the American economy.

More on AAII.com

12 Hidden Lessons From Investment History

Investors who are willing to learn from nearly a century of data can discover some important takeaways.What Market Volatility Really Is and How to Navigate It

Volatility refers to the magnitude of movement instead of a single direction; AAII founder James Cloonan encouraged investors to focus on “real risk.”Cash Is King and Free Cash Flow Wears the Crown

The just released March 2026 AAII Journal explains why free cash flow is not just an accounting exercise but is central to valuation.

AAII Sentiment Survey

Neutral sentiment among individual investors about the short-term outlook for stocks increased in the latest AAII Sentiment Survey. Meanwhile, optimism and pessimism decreased.

Bullish sentiment, expectations that stock prices will rise over the next six months, decreased 0.1 percentage points to 33.1%. Bullish sentiment is below its historical average of 37.5% for the third time in 14 weeks.

Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, increased 4.4 percentage points to 31.4%. Neutral sentiment is below its historical average of 31.5% for the 85th time in 87 weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, decreased 4.2 percentage points to 35.5%. Bearish sentiment is above its historical average of 31.0% for the fourth consecutive week.

The bull-bear spread (bullish minus bearish sentiment) increased 4.1 percentage points to –2.5%. The bull-bear spread is below its historical average of 6.5% for the fourth consecutive week.

This week’s special question asked AAII members what their perception of inflation is.

Here is how they responded:

It’s slowing, but not by enough: 38.6%

It’s returning to a more acceptable pace: 33.2%

It’s still rising too quickly: 22.4%

Not sure/no opinion: 5.4%

This week’s Sentiment Survey results:

Bullish: 33.1%, down 0.1 points

Neutral: 31.4%, up 4.4 points

Bearish: 35.5%, down 4.2 points

Historical averages:

Bullish: 37.5%

Neutral: 31.5%

Bearish: 31.0%

See more Sentiment Survey results.

AAII Asset Allocation Survey

Individual investors’ allocations to bonds increased while stock and cash allocations decreased in the February AAII Asset Allocation Survey.

Stock and stock fund allocations decreased 0.8 percentage points to 69.4%. Stock and stock fund allocations are above their historical average of 61.5% for the 69th consecutive month.

Bond and bond fund allocations increased 1.0 percentage points to 16.4%. Bond and bond fund allocations are above their historical average of 16.0% for the first time in five months.

Cash allocations decreased 0.2 percentage points to 14.2%. Cash allocations are below their historical average of 22.5% for the 39th consecutive month.

February AAII Asset Allocation Survey results:

Stocks and Stock Funds: 69.4%, down 0.8 percentage points

Bonds and Bond Funds: 16.4%, up 1.0 percentage points

Cash: 14.2%, down 0.2 percentage points

February AAII Asset Allocation Details:

Stocks: 30.7%, up 1.6 percentage points

Stocks Funds: 38.7%, down 2.4 percentage points

Bonds: 5.2%, up 0.6 percentage points

Bond Funds: 11.2%, up 0.4 percentage points

Historical averages:

Stocks/Stock Funds: 61.5%

Bonds/Bond Funds: 16.0%

Cash: 22.5%

Take the Asset Allocation Survey.